The shift from traditional messaging systems to digital asset rails is no longer a "future" concept; as of 2026, it is a structural reality. For decades, the SWIFT (Society for Worldwide Interbank Financial Telecommunication) system has been the undisputed king of cross-border finance. However, its reliance on a 1970s-era "correspondent banking" model—where money moves through multiple intermediary banks—has created significant friction.

What is Swift System?

To understand the scale of the current "crypto revolution," it is essential to first define the established giant: the SWIFT system. Established in 1973, SWIFT (Society for Worldwide Interbank Financial Telecommunication) acts as the secure messaging "nervous system" for the global financial world, connecting over 11,000 banks across 200 countries. However, a common misconception is that SWIFT moves money; in reality, it only moves instructions. The actual settlement of funds still relies on a complex web of "correspondent banking," where banks must hold massive amounts of capital in pre-funded foreign accounts (Nostro/Vostro) to fulfill those instructions.

By 2026, SWIFT is undergoing its most significant modernization in decades to stay competitive. The system has officially transitioned to ISO 20022, a data-rich messaging standard that allows for more automation and fewer manual errors. Furthermore, SWIFT has begun integrating its own blockchain-based shared ledger to orchestrate the movement of regulated digital assets. While these upgrades aim to reduce the "last mile" delays where 80% of a transaction's journey time occurs, the system still operates within a centralized, permissioned framework. This remains the fundamental divide between SWIFT’s centralized evolution and the decentralized, "trustless" nature of public crypto rails.

Today, crypto-assets and blockchain protocols are bypassing these bottlenecks, offering a parallel infrastructure that is faster, cheaper, and more inclusive.

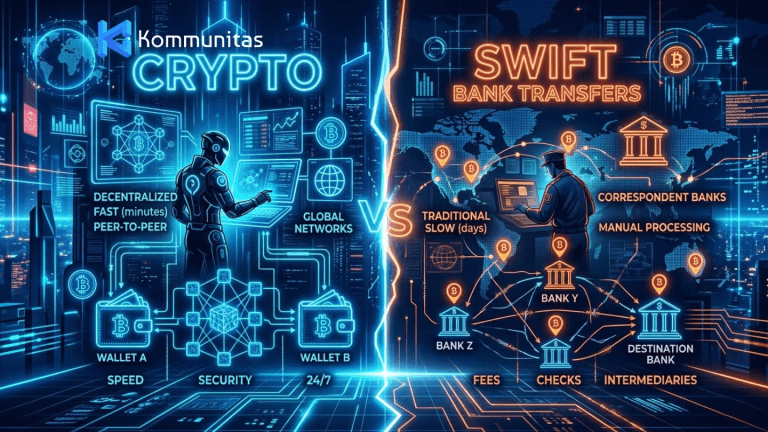

1. The Core Problem: SWIFT vs. Settlement

To understand the revolution, one must first understand that SWIFT does not actually move money. It moves messages about money.

SWIFT Model: A bank in London sends a message to a bank in New York. Actual settlement requires "Nostro" and "Vostro" accounts to be pre-funded with billions of dollars to ensure liquidity. This process typically takes 3–5 business days.

Crypto Model: Blockchain protocols combine the messaging and the settlement into a single event. When a stablecoin or token is sent, the value transfer is the message. Settlement occurs in seconds to minutes, 24/7/365.

2. Key Data: The Rise of the "Stablecoin Sandwich"

By 2026, the "Stablecoin Sandwich" has become the preferred method for B2B cross-border payments in emerging markets. This involves converting local fiat to a stablecoin, sending it across the border instantly, and off-ramping to the destination’s local currency.

The Impact of Stablecoins:

In 2025, stablecoins processed over $11.4 trillion in transaction volume. While much of this was crypto-native, "real-world" payment volume (B2B and remittances) grew by 60% year-over-year. As of Q1 2026, there are over 500 million unique wallet addresses globally, a 40% increase from 2023 levels.

3. Disruption Drivers: Why Change is Happening Now

A. Ending the "Liquidity Trap"

Traditional banks keep roughly $10 trillion in capital "trapped" in pre-funded accounts globally just to make SWIFT work. Protocols like Ripple (XRP) and Solana (PayFi) allow banks to use digital assets as "bridge currency," releasing that capital for more productive uses.

B. The 2026 Regulatory Breakthrough

The era of "The Wild West" is largely over. Major frameworks are now active:

MiCA (EU): Provides a clear legal path for euro-backed stablecoins.

The GENIUS Act (US): Legally recognizes "permitted stablecoin issuers," treating dollar-backed tokens as legitimate money rather than speculative investments.

C. Financial Inclusion

In corridors like the US-to-Philippines or UAE-to-India, traditional remittances cost an average of $12 per $200 sent. Blockchain-based apps have slashed this to under $2, putting billions back into the hands of migrant workers and SMEs.

4. The Future: Coexistence or Replacement?

While the narrative often pits Crypto against SWIFT, 2026 has seen a trend of convergence.

SWIFT’s Evolution: SWIFT itself has integrated blockchain-based shared ledgers to its infrastructure to enable 24/7 movement of regulated tokenized value.

The Hybrid Model: Many institutions now use SWIFT for messaging in high-compliance jurisdictions while using blockchain rails for the actual movement of value to avoid the delays of correspondent banking.

Final Verdict

The "revolution" is not just about a new type of money; it’s about a new type of railway. By removing the middleman and turning "money" into "data," blockchain technology has effectively ended the era of waiting five days for your own funds to cross a border.

Data Note: Current 2026 projections by Citigroup suggest that by 2030, the stablecoin supply will reach between $1.9 trillion and $4 trillion, potentially handling 10% of all global retail payments.

Learn more in our guide on Polygon Vs BSC.